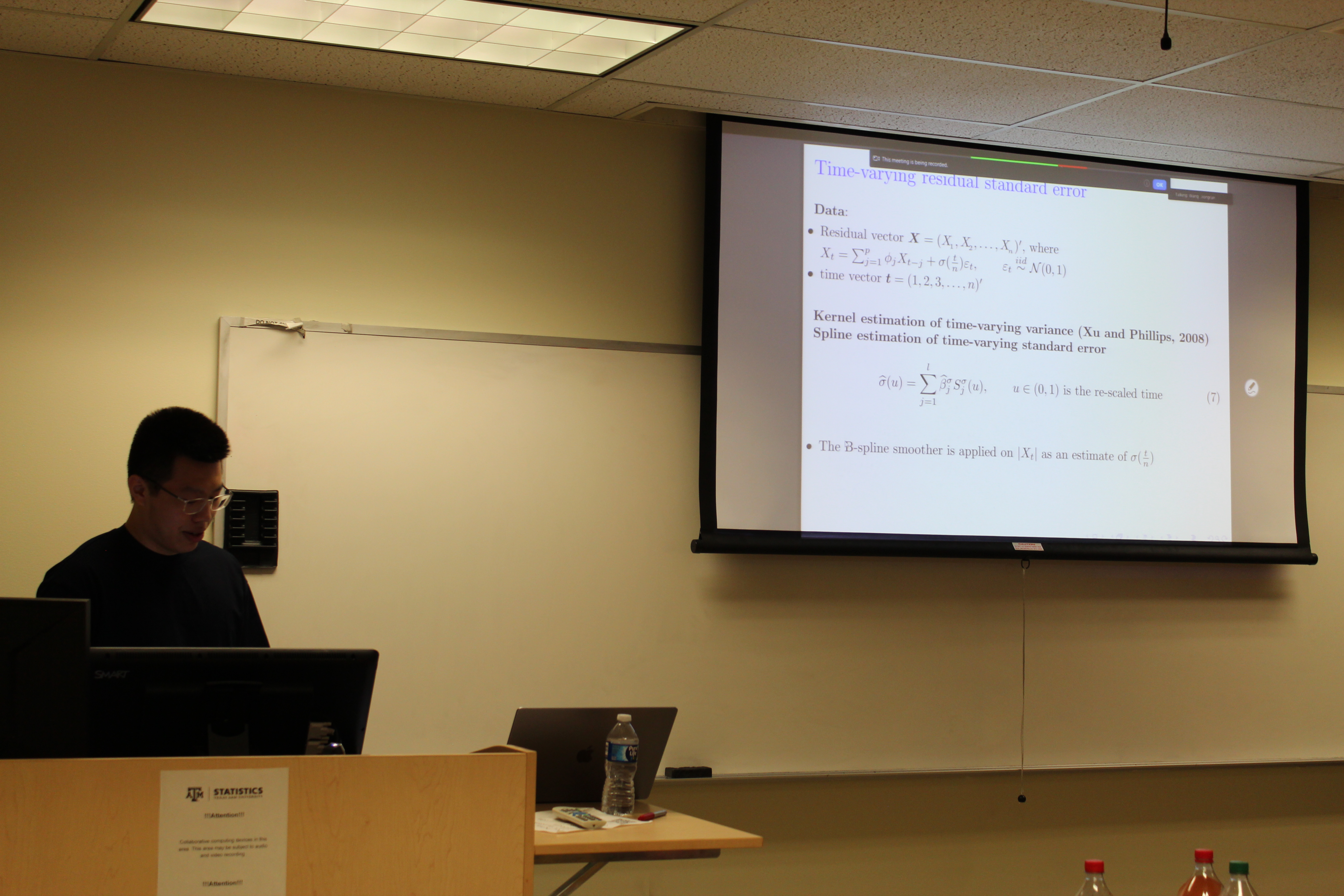

Stat Cafe - Qiyuan Wang

Detecting Stellar Flares with Conditional Volatility

- Time: Wednesday 10/2/2024 from 11:30 AM to 12:30 PM

- Location: BLOC 411

- Pizza and drinks provided

Description

For more than forty years now, discrete-time models have been developed to reflect the so-called stylized features of financial time series. These properties, which include tail heaviness, asymmetry, volatility clustering and serial dependence without correlation, cannot be captured with traditional linear time series ARMA. Continuous-time ARMA (CARMA) are the continuous-time version of the well-known ARMA models, and they are convenient for modeling astronomical data, which are often unequally spaced in time. In this talk we will review ARMA and CARMA models and their application in astrophysics. We then present a novel and powerful method to analyze time series to detect flares in TESS light curves. First, we remove the trend using a time-varying deterministic harmonic fit so to capture changes in the deterministic amplitude of the light curve. Then we enlighten the analogy between the stochastic part of the light curves and GARCH processes. We demonstrate that flares can be detected as significantly large deviations from the baseline. We apply the method on exemplar light curves from two flaring stars, and discuss some of the diagnostics that become amenable to measurement.

Presentation

Recording

Gallery